No Rate Cut: Powell’s Steady H...

30 January 2025 | 4:30 am

Arthur Hayes, the Chief Investment Officer at Maelstrom and co-Founder as well as former CEO of BitMEX, has published a new essay titled “The Ugly,” in which he contends that Bitcoin could be poised for a profound near-term pullback before ultimately marching to unprecedented highs. While retaining his characteristic bluntness, Hayes lays out two scenarios when to buy Bitcoin.

Hayes’ essay begins by recounting a sudden shift in sentiment that caught him off guard. Comparing financial analysis to backcountry skiing on a dormant volcano, Hayes recalls how the mere hint of avalanche danger once forced him to stop and reassess. He expresses a similarly uneasy feeling about current monetary conditions, an intuition he says he last felt in late 2021, right before the crypto markets collapsed from their record highs.

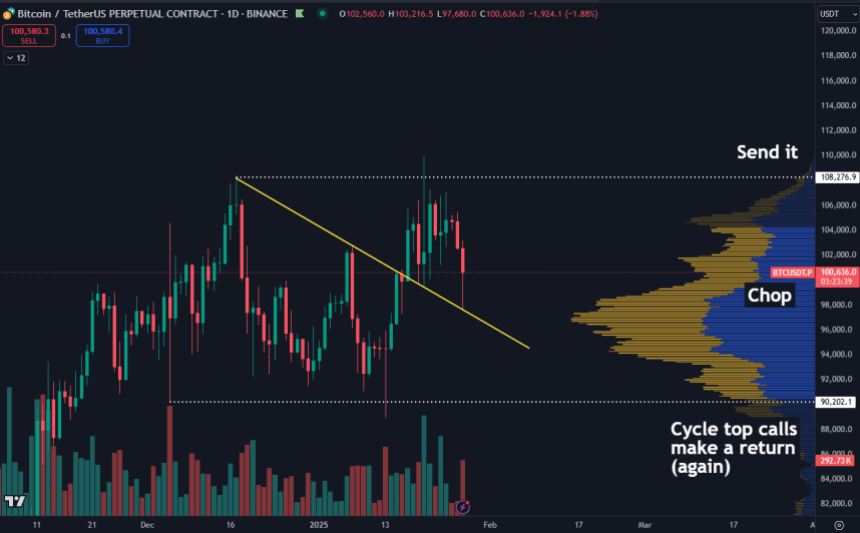

“Subtle movements between central bank balance sheet levels, the rate of banking credit expansion, the relationship between the US 10-yr treasury/stocks/Bitcoin prices, and the insane TRUMP memecoin price action produced a pit in my stomach,” he writes, emphasizing that these signals collectively remind him of the market’s precarious situation prior to the 2022 and 2023 downturns. He clarifies that he does not believe the broader bull cycle is finished, but he anticipates that Bitcoin could drop to somewhere around the $70,000 to $75,000 range before rallying sharply to reach $250,000 by year’s end.

He describes this range as plausible given that equity markets and treasury markets appear, in his words, deeply entangled in a “filthy fiat” environment still grappling with the vestiges of inflation and rising interest rates. Hayes points out that Maelstrom, his investment firm, remains net long while simultaneously raising its holdings in the USDe stablecoins to buy back Bitcoin if price falls below $75,000.

In his view, scaling back risk in the short term allows him to preserve capital that can later be deployed when a genuine market liquidation occurs. He identifies a 30% correction from current levels as a distinct possibility, while also acknowledging that the bullish momentum could continue. “if Bitcoin trades through $110,000 on strong volume with an expanding perp open interest, then I’ll throw in the towel and buy back risk higher,” he writes on his second scenario.

In attempting to decipher why a temporary pullback might happen, Hayes asserts that major central banks—the Federal Reserve in the United States, the People’s Bank of China, and the Bank of Japan—are either curbing money creation or, in some cases, outright raising the price of money by permitting yields to rise. He believes that these shifts could choke off speculative capital that has elevated both stocks and cryptocurrencies in recent months.

His discussion of the US focuses on two interlocked perspectives: that ten-year treasury yields could rise to a zone between 5% and 6%, and that the Federal Reserve, while hostile to Donald Trump’s administration, will not hesitate to reinitiate printing if it becomes essential to preserve American financial stability.

However, he believes that at some point, the financial system will need an intervention—most likely an exemption to the Supplemental Leverage Ratio (SLR) or a new wave of quantitative easing. He contends that the reluctance or slowness of the Fed to take these steps increases the probability of a near-term bond market sell-off, which could weigh on equities, and by correlation, Bitcoin.

His political analysis homes in on the lingering enmity between Trump and Federal Reserve Chair Jerome Powell, as well as the Fed’s willingness to forestall a crisis during the Biden presidency. He cites statements from former Fed governor William Dudley and references Powell’s press conference remarks that suggested the Fed might alter its approach based on Trump’s policies.

Hayes describes these tensions as a backdrop for a scenario in which Trump might allow a mini-financial crisis to unfold, forcing the Fed’s hand. Under such stress, the Fed would have little choice but to prevent a broader meltdown, and monetary expansion could then follow. He suggests that it would be politically expedient for the Trump administration to permit yields to surge to crisis levels if it meant that the Fed would be compelled to pivot into the large-scale money printing that many in crypto circles expect.

China, Hayes remarks, had seemed poised to join the liquidity party with an explicit reflation program until a sudden U-turn in January, when the PBOC halted its bond-buying program and allowed the yuan to stabilize in a stronger position. He attributes this policy change to internal political pressures or possibly strategic maneuvering for future negotiations with Trump.

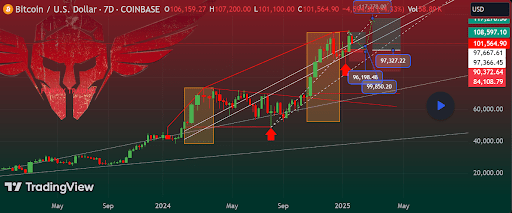

Hayes also acknowledges that some readers might find the correlation between Bitcoin and traditional risk assets perplexing, given the long-term argument that Bitcoin is a unique store of value. Yet he points to charts showing a rising 30-day correlation between Bitcoin and the Nasdaq 100.

In the short term, he says, the leading cryptocurrency remains sensitive to changes in fiat liquidity, even if the coin ultimately trades on an uncorrelated basis over extended time horizons. He thus portrays Bitcoin as a leading indicator: if bond yields spike and equity markets tumble, Bitcoin could begin its dive before tech stocks follow. Hayes thinks that once authorities unleash renewed monetary stimulus to quell volatility, Bitcoin would be the first to bottom out and rebound.

He admits that predicting exact outcomes is impossible and that any investor must play perceived probabilities rather than certainties. His decision to hedge is derived from the concept of expected value. If he believes there is a substantial chance of a 30% pullback versus a smaller probability that Bitcoin will continue higher before he decides to buy back in at a 10% premium, reducing exposure still yields a better risk-reward ratio.

“Trading isn’t about being right or wrong,” he emphasizes, “but about trading perceived probabilities and maximizing expected value.” He also underscores that this protective stance allows him to wait for the kind of dramatic liquidation move in altcoins that often accompanies a short-term Bitcoin collapse, a scenario he calls “Armageddon” in the so-called “shitcoin space.” In such circumstances, he wants ample funds available to pick up fundamentally sound tokens at severely depressed prices.

At press time, BTC traded at $102,530.

30 January 2025 | 4:30 am

30 January 2025 | 9:30 pm

30 January 2025 | 2:30 pm

30 January 2025 | 12:30 pm

30 January 2025 | 5:30 pm

30 January 2025 | 9:08 pm